Q1 2026 SFR Rental Acquisitions Overview

Rust Belt Surging; Gross Yields Inch Higher

We looked at single-family residential rental purchases in Q1 2026 to see where the most single family rental investment activity is, how it’s changing compared to prior periods, and more.

A quick note on methodology: this isn’t an exhaustive view of every single family rental purchased in Q1 2026, but only those for which we had rental price data.

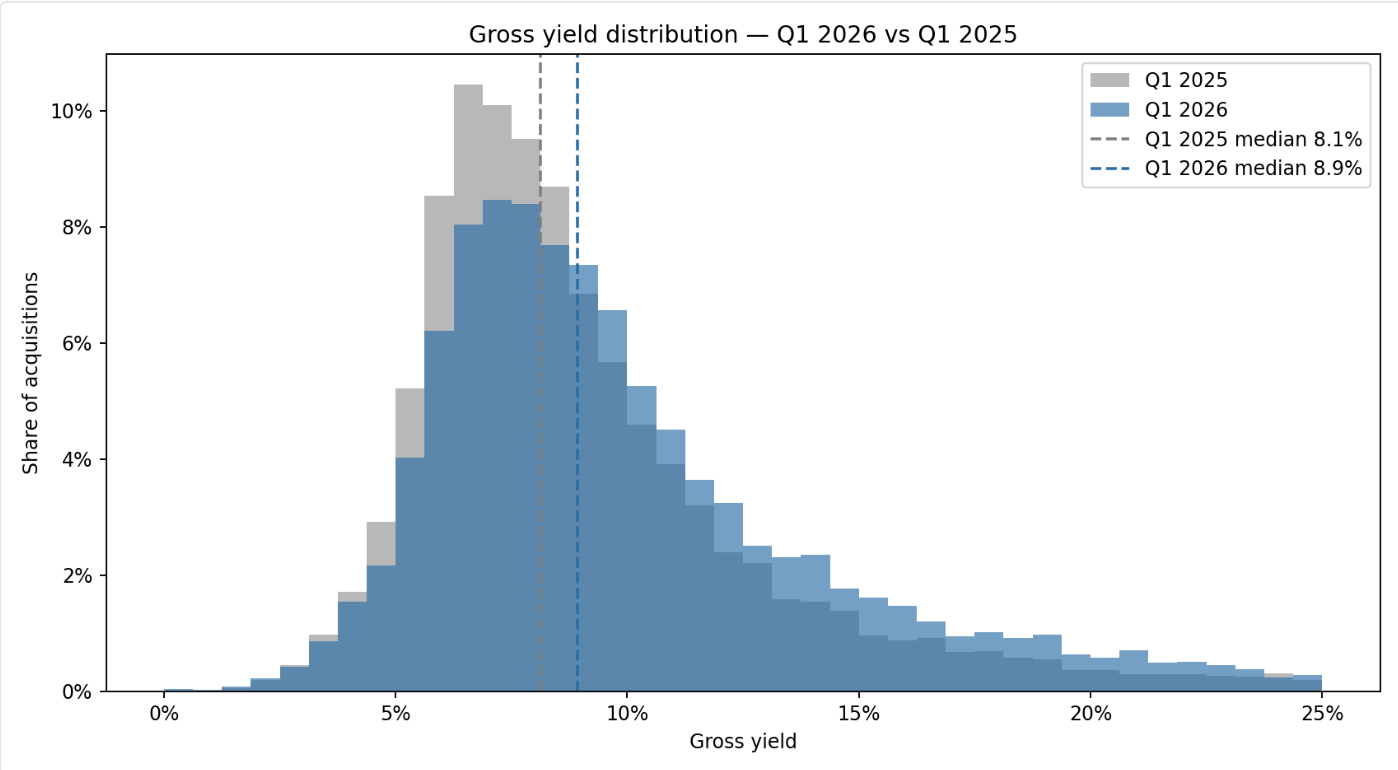

Median gross yield for newly acquired single family rental properties rose from 8.1% to 8.9% comparing Q1 2025 to Q1 2026, marking a shift towards higher yielding rental properties.

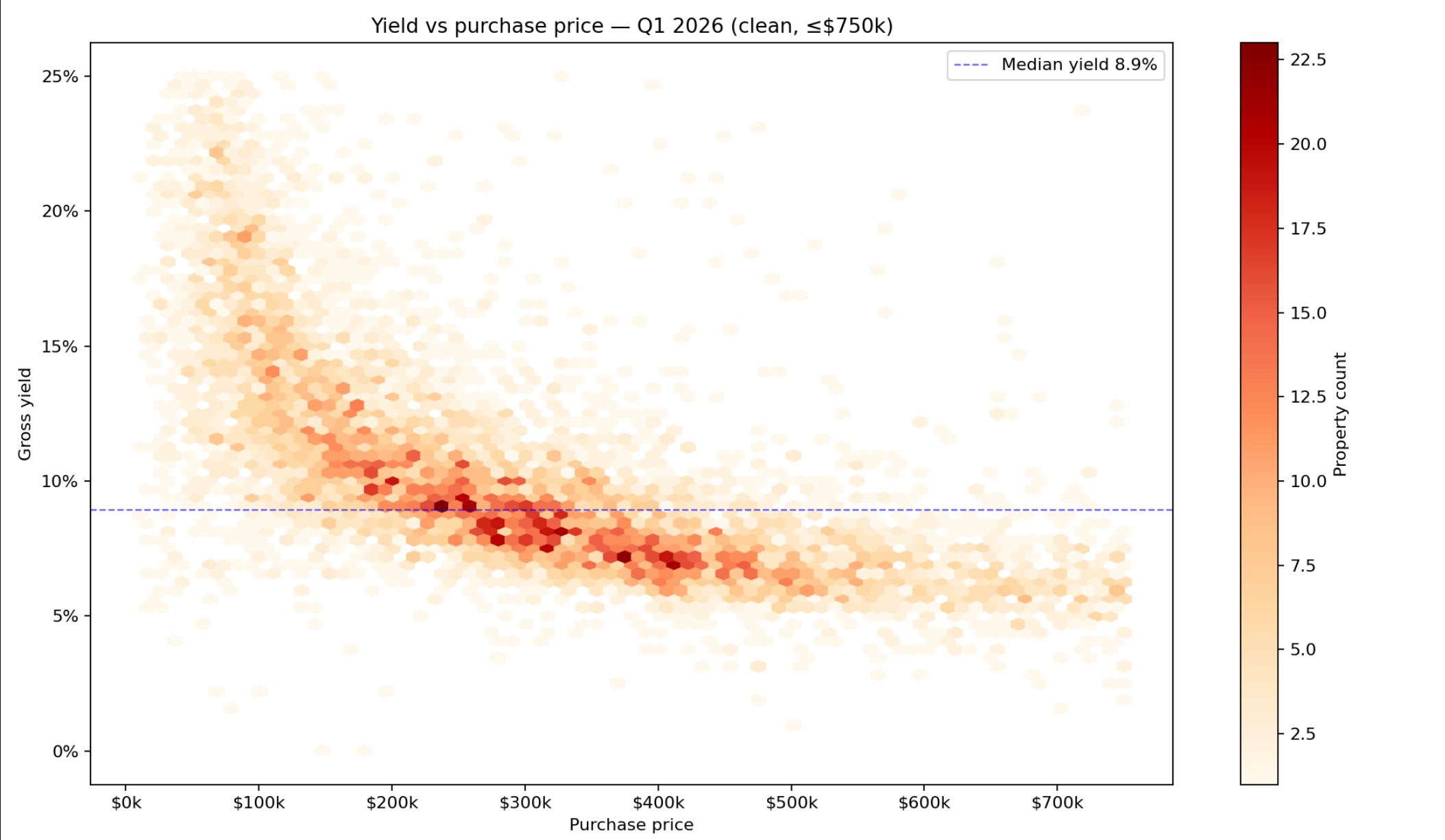

While nationwide aggregates are interesting, when comparing purchase price to gross yield it’s clear investors adopt many different strategies — everything from high gross yield but low-cost properties that may have higher percent of expenses needed to very low yielding properties in high cost of living areas.

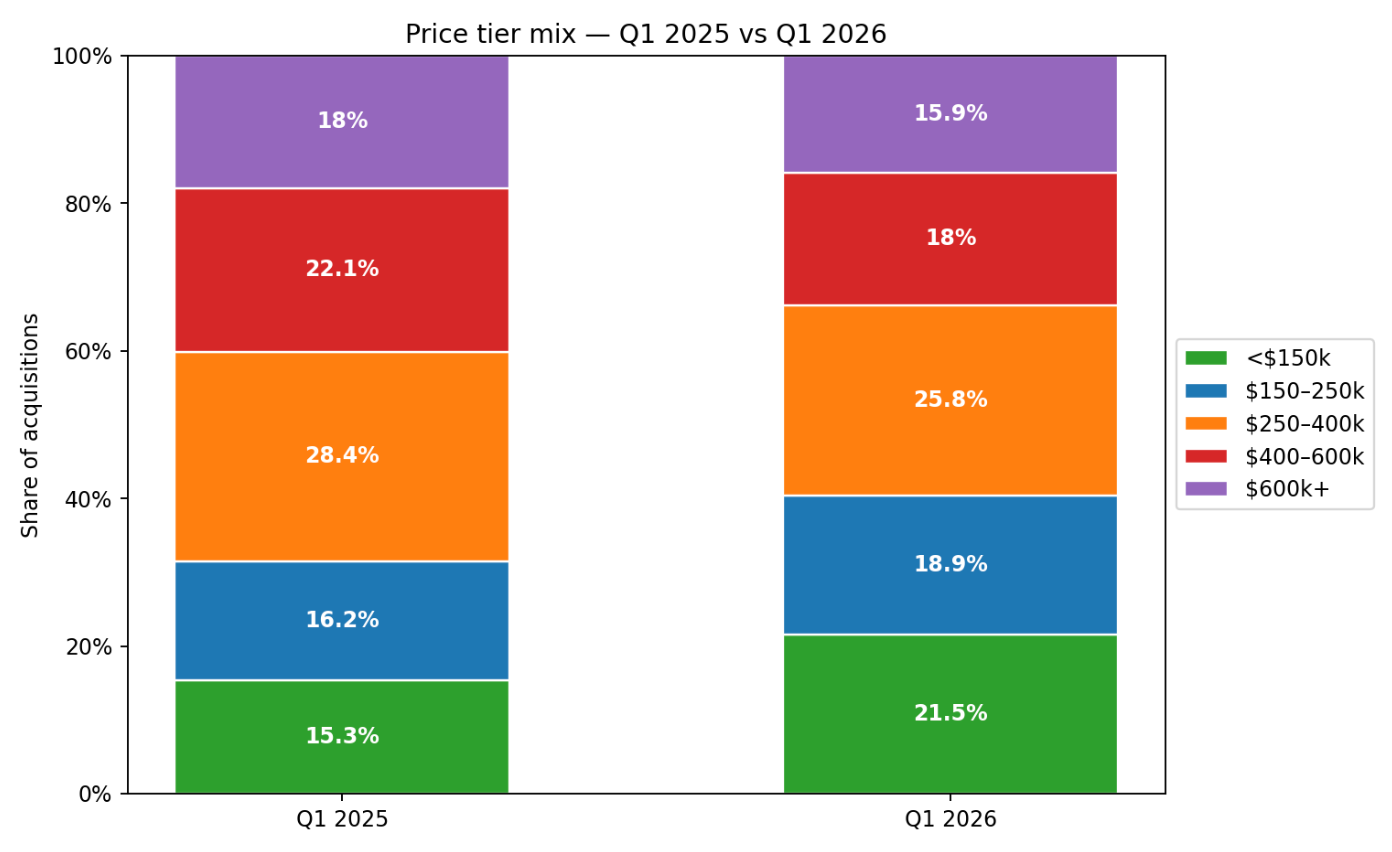

The increase in yield was mostly due to a shift in type of properties being acquired with less expensive homes making up a larger share of the percent of properties acquired.

Eight of the top ten metros that saw the largest increase in acquisitions were regions that had an average acquisition price below $250k, while all ten of the largest MSA decliners had an average acquisition price above $250k.

Looking to do this type of analysis yourself? Reach out to get setup with our ChatGPT/Claude plugin!

You can access the underlying data directly via MCP. Bulk data on nationwide rental listings and investor purchases is also available for purchase. Respond to this email if interested in learning more.

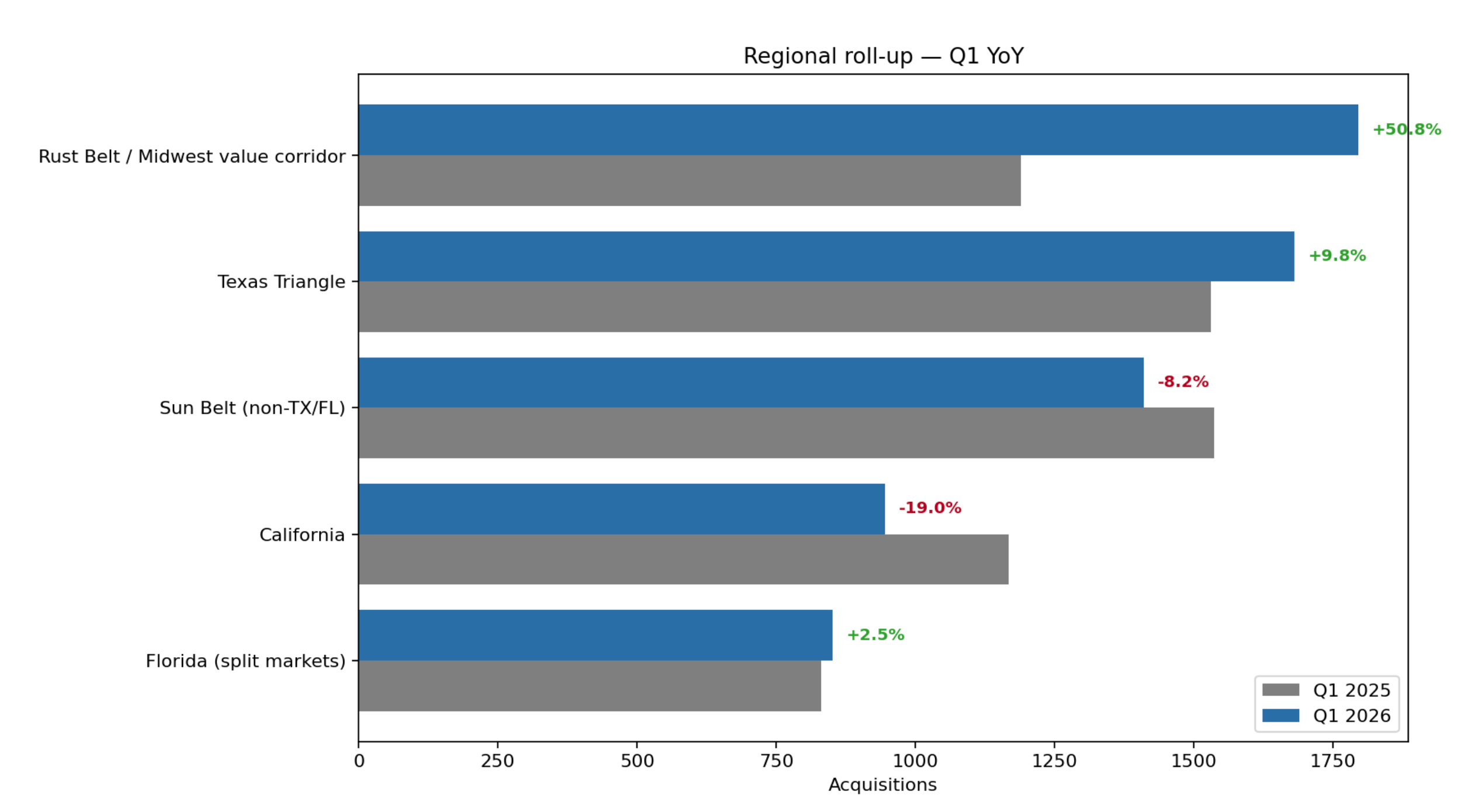

Regional patterns

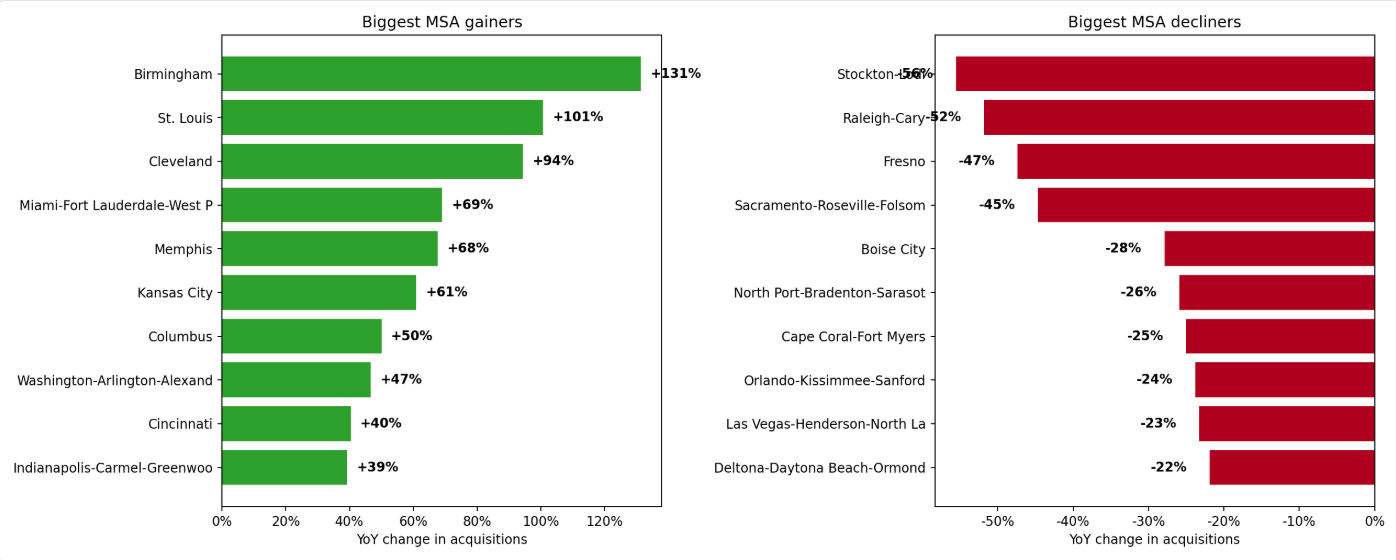

Looking at major regions, the Rust Belt is experiencing the largest increase in activity with the major Texas markets also performing strongly. Outside of Austin (down 11%), San Antonio, DFW, and Houston all saw positive growth.

California saw new rental acquisitions decline sharply and Florida as a whole was roughly even, but highly dependent on market. Miami +69% and Palm Bay +61% were pulling up the numbers while Orlando −24%, Cape Coral −25%, and Sarasota −26% pulled down.

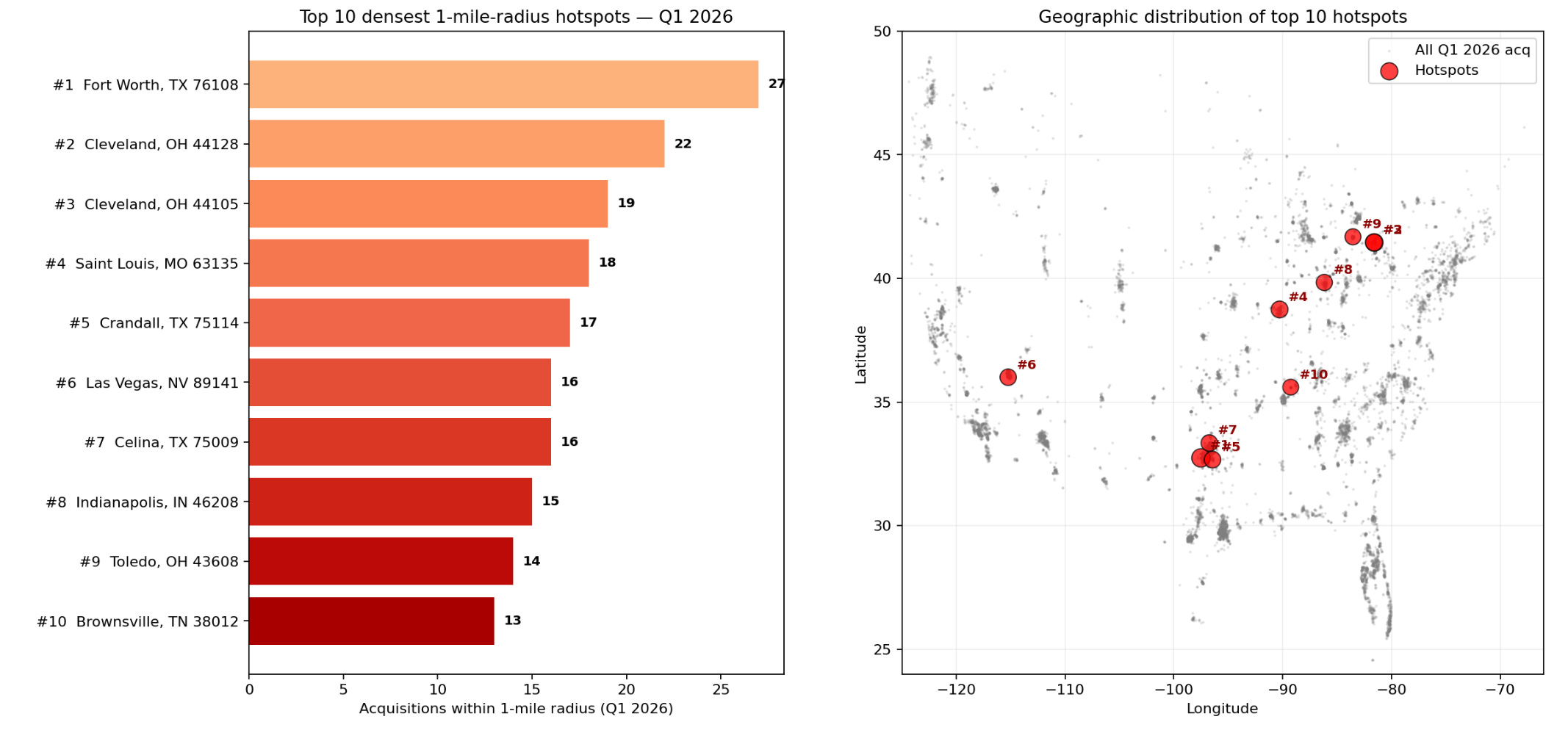

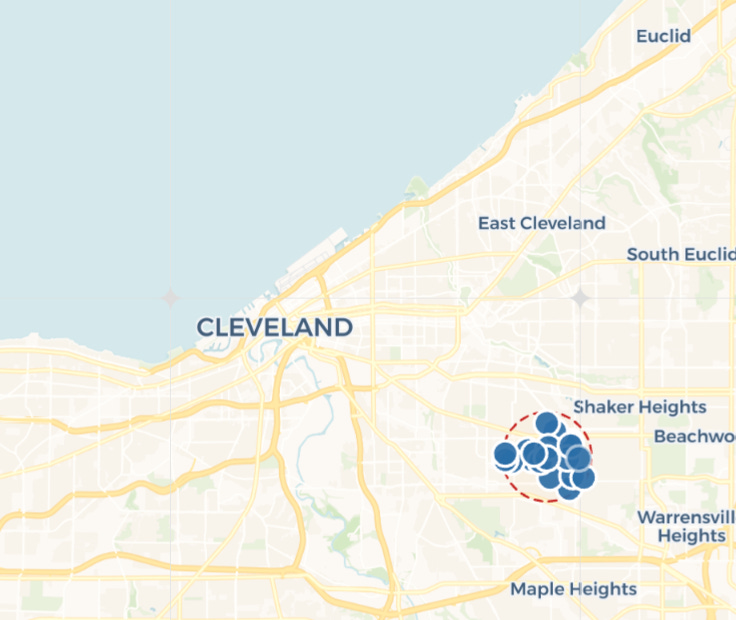

Finally, we looked at the densest one-mile radius spots to see which neighborhoods investors are buying in.

Note: given we’re looking at only a subset of rental acquisitions for a single quarter, portfolio acquisitions may skew metrics.

Diving into individual hotspots can reveal interesting behavior. In some you’ll find institutional investors buying blocks of new construction vs others where there are dozens of unique buyers.

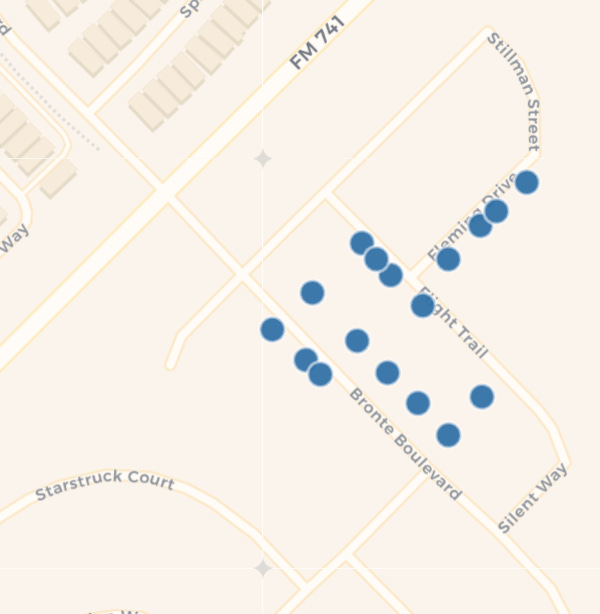

In the Crandall, Texas hotspot, Invitation Homes bought a handful of new construction properties that they’re renting out.

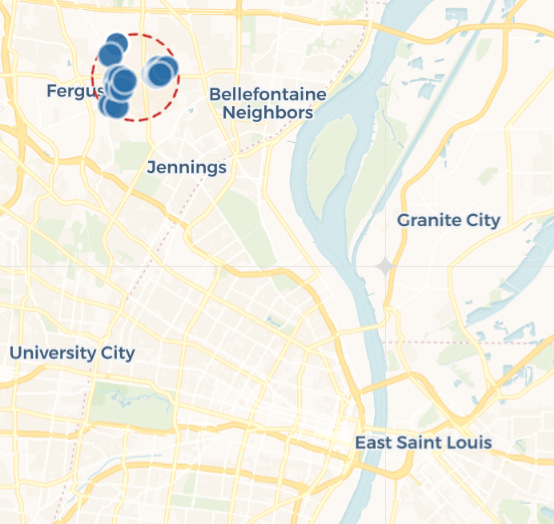

The Ferguson and Cleveland hotspots are the opposite and have a diverse set of investors purchasing throughout nearly every block in the neighborhood.

If you’d like access to the underlying data, please reach out by replying to this email.