Opendoor Q1 2024 Earnings

Opendoor beat guidance, delivering on prioritizing operational rigor.

Executive Summary

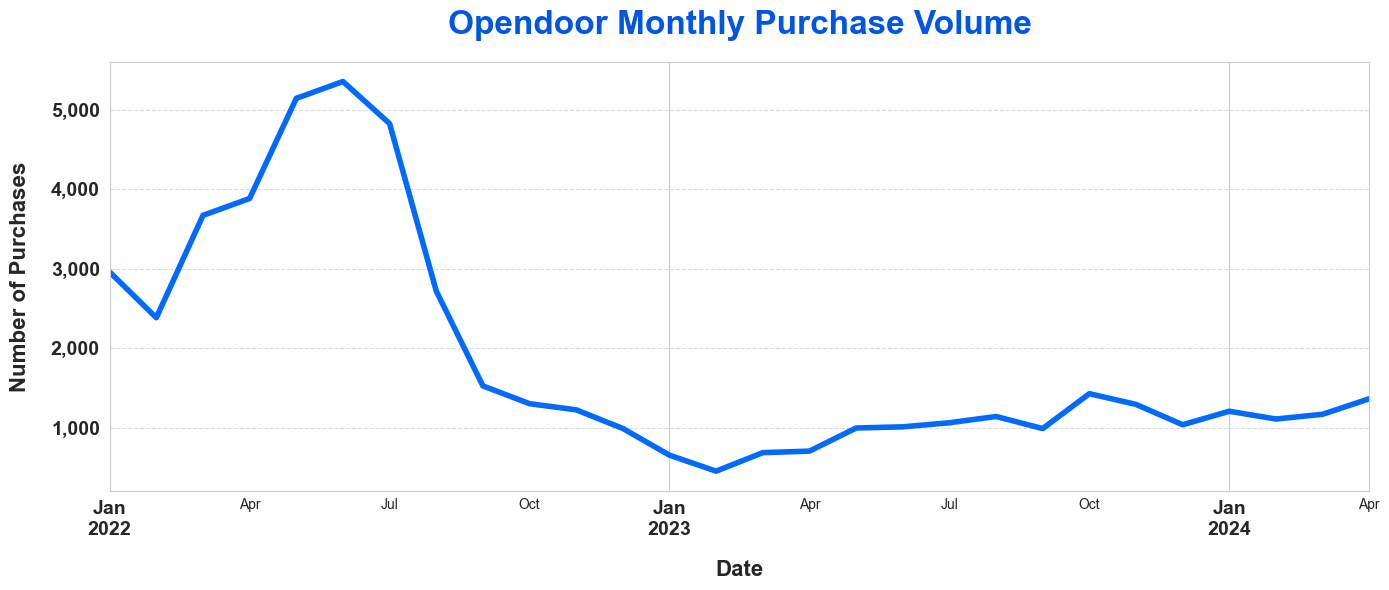

Opendoor's Q1 results exceeded the high end of guidance across revenue, Contribution Margin, and Adjusted EBITDA. Purchase volume increased significantly year-over-year, with the company purchasing 3,458 homes in Q1, up 98% vs Q1 2023. However, this is still well below peak 2022 purchase volumes of 5,000+ homes per month.

The company has guided to purchase 4,500+ homes in Q2 2024, which would represent a substantial increase over the 2,680 purchased in Q2 2023. Opendoor also established a new $200 million ATM (at-the-market) equity program, providing financial flexibility to opportunistically fund growth over the next three years.

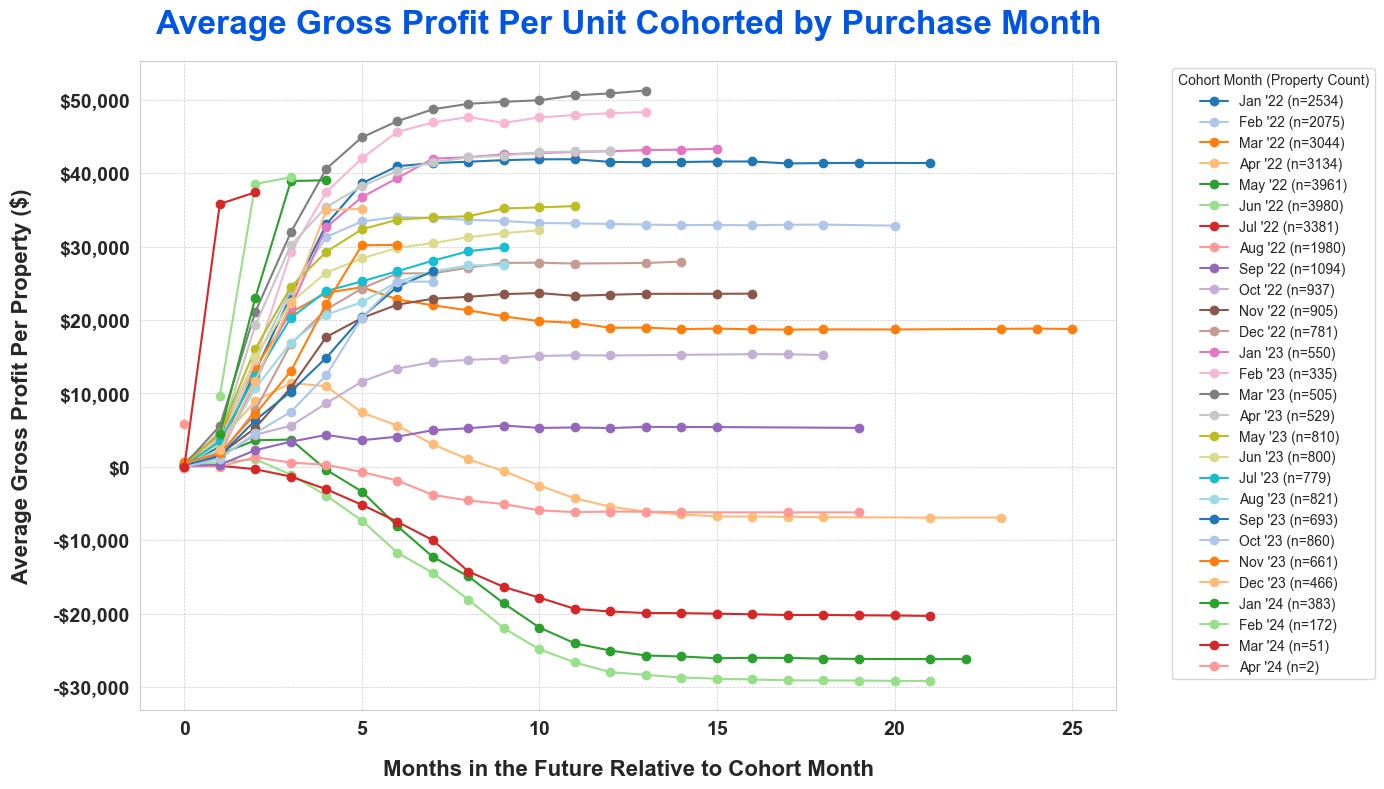

Opendoor has been able to sustain improved unit economics while growing purchase volume, generating $25k+ in spread profit per home across properties purchased in the second half of 2023. Detailed metro-level profit breakdowns of the most recent cohorts are available for paid subscribers at the end of this article.

A key industry development during the quarter was the proposed settlement of antitrust lawsuits against the National Association of Realtors (NAR) related to agent commissions. Under the settlement, effective August 2024, seller's agents could no longer specify buyer's agent commissions on MLS listings, and buyers would negotiate compensation directly with their agent. Opendoor's management believes the NAR settlement will provide consumers with more transparency and choice, driving a trend towards lower transaction costs. CEO Carrie Wheeler stated, "If commissions do decline, Opendoor may be able to pass these cost savings back to consumers in the form of lower spreads," potentially resulting in more direct transactions through platforms like Opendoor. The company's business model doesn't rely on buyer's agent commissions, which are currently a cost when reselling homes.

Introduction

In Q1 2024, Opendoor purchased 3,458 homes, an increase of 98% year-over-year but a decrease of 6% quarter-over-quarter. 3,078 homes were sold, generating $1.18 billion in revenue, above the guided range of $1.0-$1.1 billion. Gross profit was $114 million, representing a 9.7% gross margin, ahead of 8.3% in Q4 2023. Contribution profit was $57 million, a 4.8% Contribution Margin, exceeding the 3.4% Contribution Margin in Q4.

As explored in previous analyses of Opendoor's business, the company faced significant challenges with homes purchased in early 2022. Since then, purchase volume has been drastically reduced while the company adjusts its buy box and navigates the new interest rate environment. So far, Opendoor has sustained the improvements it made to unit economics while growing purchase volume. The company's partnership with eXp Realty, launched in February 2024, is expected to broaden its reach and boost brand awareness among agents.

A key industry development since Opendoor's last earnings call was the proposed settlement of multiple antitrust lawsuits against the National Association of Realtors (NAR) related to agent commissions. The lawsuits alleged that NAR rules, particularly the cooperative compensation requirement for listing on the Multiple Listing Service (MLS), inflated commissions and reduced competition. Under the settlement, set to take effect in August 2024, seller's agents would no longer be able to specify the buyer's agent commission on MLS listings, and buyers would instead negotiate compensation directly with their agent. Opendoor's management views this settlement positively, believing it will provide consumers with more transparency and choice in real estate transactions. CEO Carrie Wheeler stated, "We believe this settlement represents an important positive change for our industry by giving consumers more transparency and choice on how they transact in the housing market." Importantly, Opendoor's business model does not rely on earning revenue from buyer's agent commissions, which Wheeler noted "are a cost to us today, which we pay when we resell our homes." The company believes the settlement will drive a long-term trend towards lower transaction costs. "If commissions do decline, Opendoor may be able to pass these cost savings back to consumers in the form of lower spreads," Wheeler explained, potentially resulting in more transactions as consumers opt to transact directly through platforms like Opendoor rather than listing on the MLS. As Opendoor continues to focus on providing a differentiated customer experience, leveraging its direct buying and selling platform, and generating positive unit economics while scaling, it is well-positioned to capitalize on these potential shifts in consumer behavior and deliver profitability at scale.

Data Overview

SFR Analytics has a uniquely detailed view into the performance of Opendoor’s business through a two step process:

Entity matching and reconciliation

Ex: All legal entities like “OPENDOOR C LLC”, “OPENDOOR D LLC”, etc. are identified and linked back to Opendoor

Processing of nationwide deed and assessor data, updated daily

For all home sales nationwide, datapoints like the buyer, seller, sale date, sale amount, loan amount, property address, etc.

The combination of complete entity matching and reconciliation with daily updated deed and assessor data means visibility into all of Opendoor’s purchase and sale activity at the transaction level.

Analysis & Results

Opendoor (NASDAQ: OPEN) has had a difficult time in the public markets since listing via a SPAC in December 2020, with the stock trading down as much as 95% from the highs it reached in February 2021.

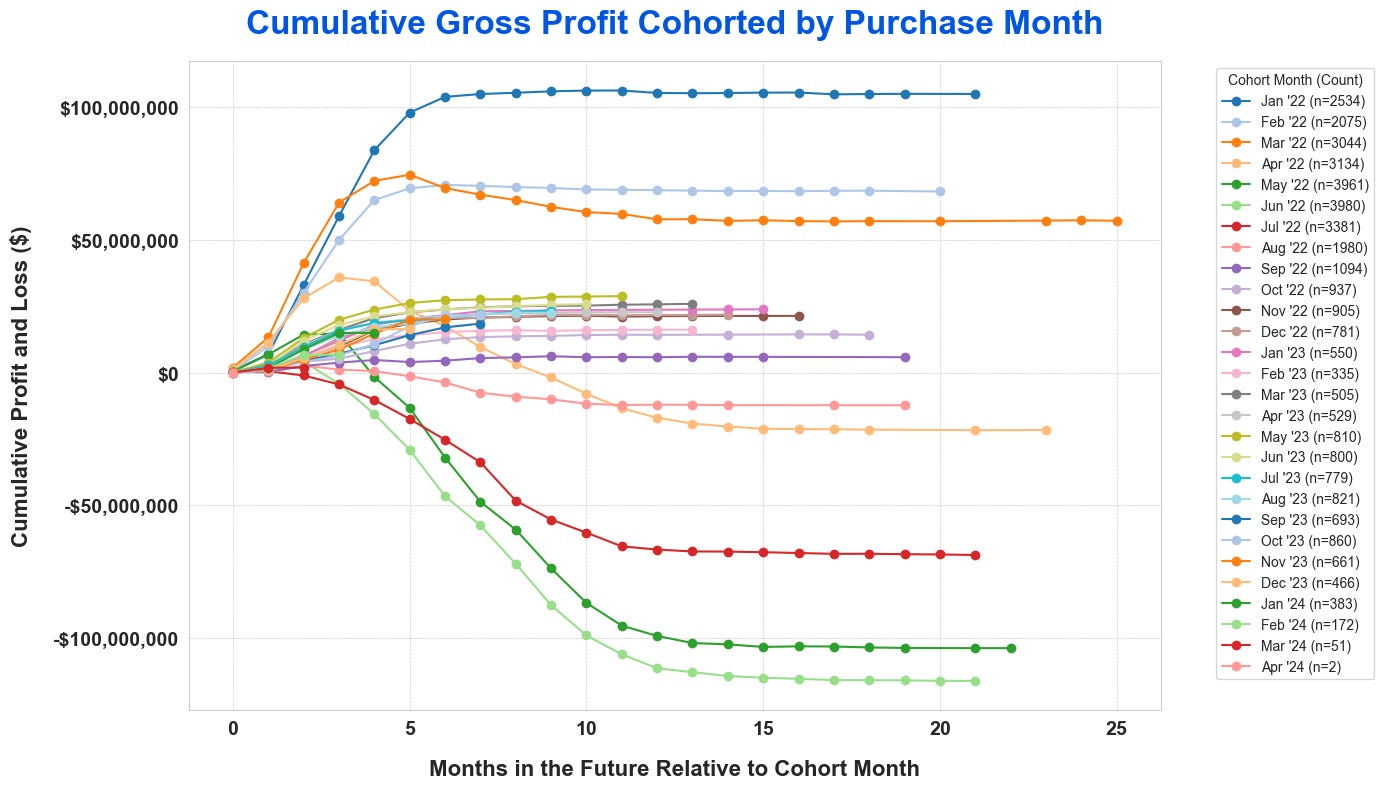

At a high level, the purchase volume and cohort curve charts paint a clear picture: Opendoor acquired a lot of homes in early 2022, and it didn’t work out well. Across the 5,000+ homes acquired in each of May and June, we estimate that Opendoor lost an average of $25k+ per home on the spread difference between purchase price and sale price. Framed differently, we estimate that Opendoor generated $100m+ in gross margin losses for each of these cohorts.

Starting in July 2022, the company quickly pumped the brakes on acquisition volume, acquiring fewer than 1,000 homes per month by the end of 2022, and keeping close to that pace throughout 2023, with a slight uptick in October 2023. While Opendoor slowed acquisition volume significantly, along the way it also improved its unit economics, reversing its gross margin losses with homes purchased in Jan 2023 through April 2023 generating $40k+ in gross margin profit per home.

It’s worth noting, however, that Opendoor’s performance varied significantly by time period and market, a topic explored further in the section Market-Level Breakdown & Future Outlook. In Phoenix, for example, Opendoor’s gross profit per property has swung over $100,000+ between the between 2022 and 2023 cohorts.

Note: properties in non-disclosure states have been excluded from the gross margin cohorts, due to limited price information available, see footnote for additional details.

Purchase Volume

On its Q4 2023 earnings call, management indicated that the company would return to growing purchase volume. That effort is reflected in the numbers to date, with transaction volume growing gradually month-over-month to reach almost 1,400 in April. Other than in October 2023, Opendoor hadn’t purchased this many homes in a month since September 2022.

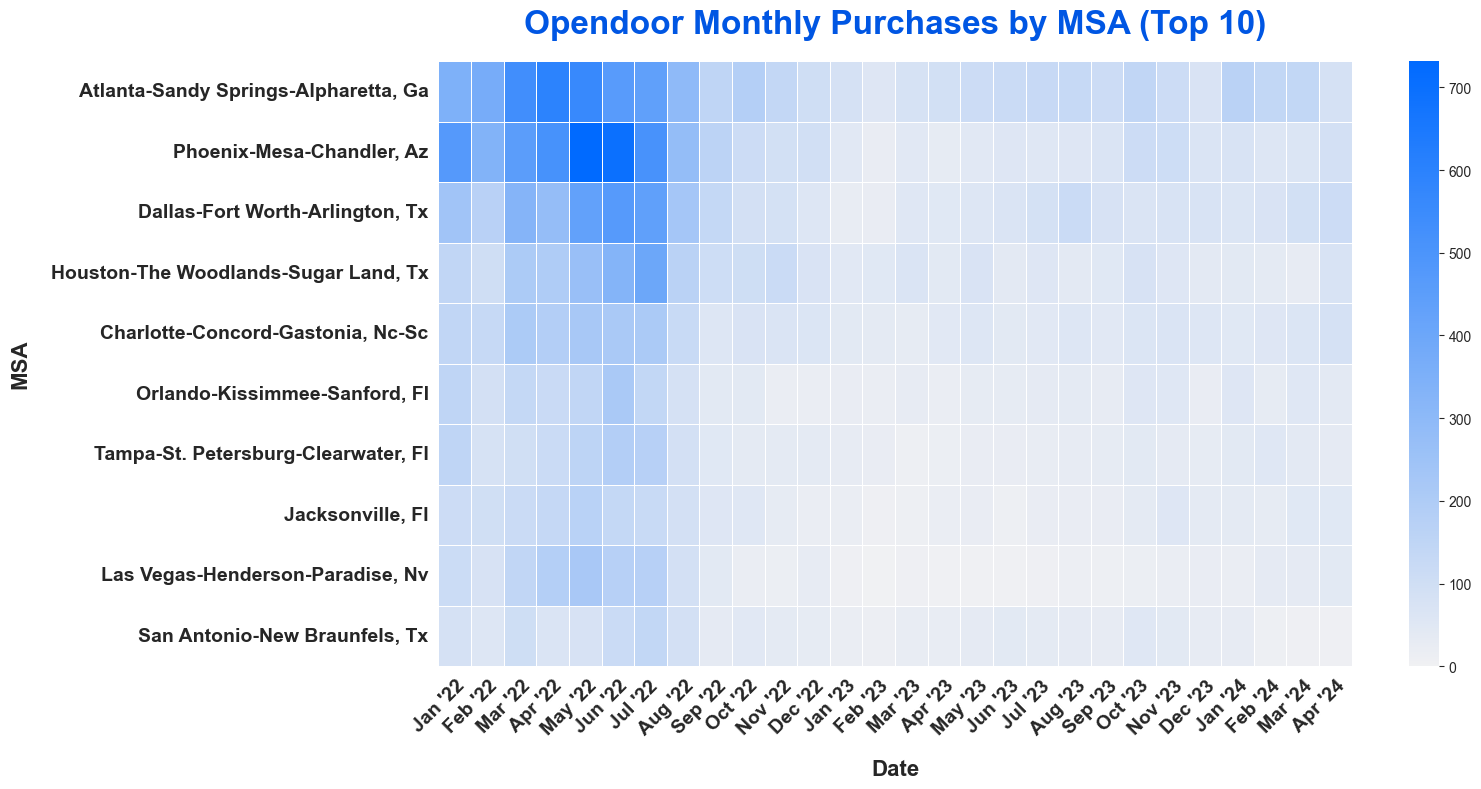

In Q1 2024, Atlanta was the metro where Opendoor purchased the most homes. Trends in purchase volume varied by geography, along with unit-level performance, a topic explored further in the section Market-Level Breakdown & Future Outlook.

Gross Profit

Market conditions changed quickly for Opendoor’s business: while Jan 2022 - March 2022 were gross margin profitable cohorts, losses mounted quickly, with slight losses in the April 2022 cohort turning into $100m+ in gross margin losses for each of the May 2022 and June 2022 cohorts, and more than $50m in gross margin losses in July 2022. Since slowing the bleeding with a slightly negative August 2022 cohort, Opendoor has generated gross margin profits in each cohort from September 2022 to present; however, lower purchase volume for these cohorts means that they’ve contributed less total gross profit, posting between $15m and $25m, compared to $50m+ each in Jan 2022, Feb 2022, and March 2022.

Unit-Based Gross Profit

While Opendoor’s lower purchase volume means that recent cohorts haven’t generated as much absolute gross profit as early 2022 cohorts, they’ve been some of the best on record on a unit basis, generating $40k+ in gross margin per property.

Market-Level Breakdown & Future Outlook

While Opendoor struggled in 2022, its performance wasn’t evenly distributed across cities. In fact, while some cities struggled mightily, others held up relatively well. Changes in Opendoor’s purchase mix as well as commentary from management on recent earnings calls suggest what’s to come for the company.

Note: the remainder of this article is available to paid subscribers, sign up below for access. Paid subscribers get full access to weekly data-rich articles about the SFR market and select additional articles only available to paid subscribers.