Opendoor Facts & Figures

Opendoor is up 500%+ this month, let's look at the data

Opendoor’s stock hit a 12-month high of $4.97 per share on Monday before quickly dropping to $3.21 to end the day. This marks a 500%+ increase in value over the last four weeks for the iBuyer. While the fervor is strong (it was the most traded stock on Monday and received a record number of social media mentions), we wanted to dive into the underlying data to take a closer look at performance.

In February 2021, Opendoor hit an all time high of $39.24. In June 2024, Opendoor hit an all time low price of $0.51. Back in 2022, markets reacted poorly as Opendoor went gross margin negative (meaning on average they sold homes for a lower price than what they purchased them for) while interest rates increased rapidly.

Zillow and Redfin put a halt to their iBuying business lines, iBuyer transaction volume declined significantly, and housing headwinds from rapidly increasing interest rates made for a difficult environment to operate in.

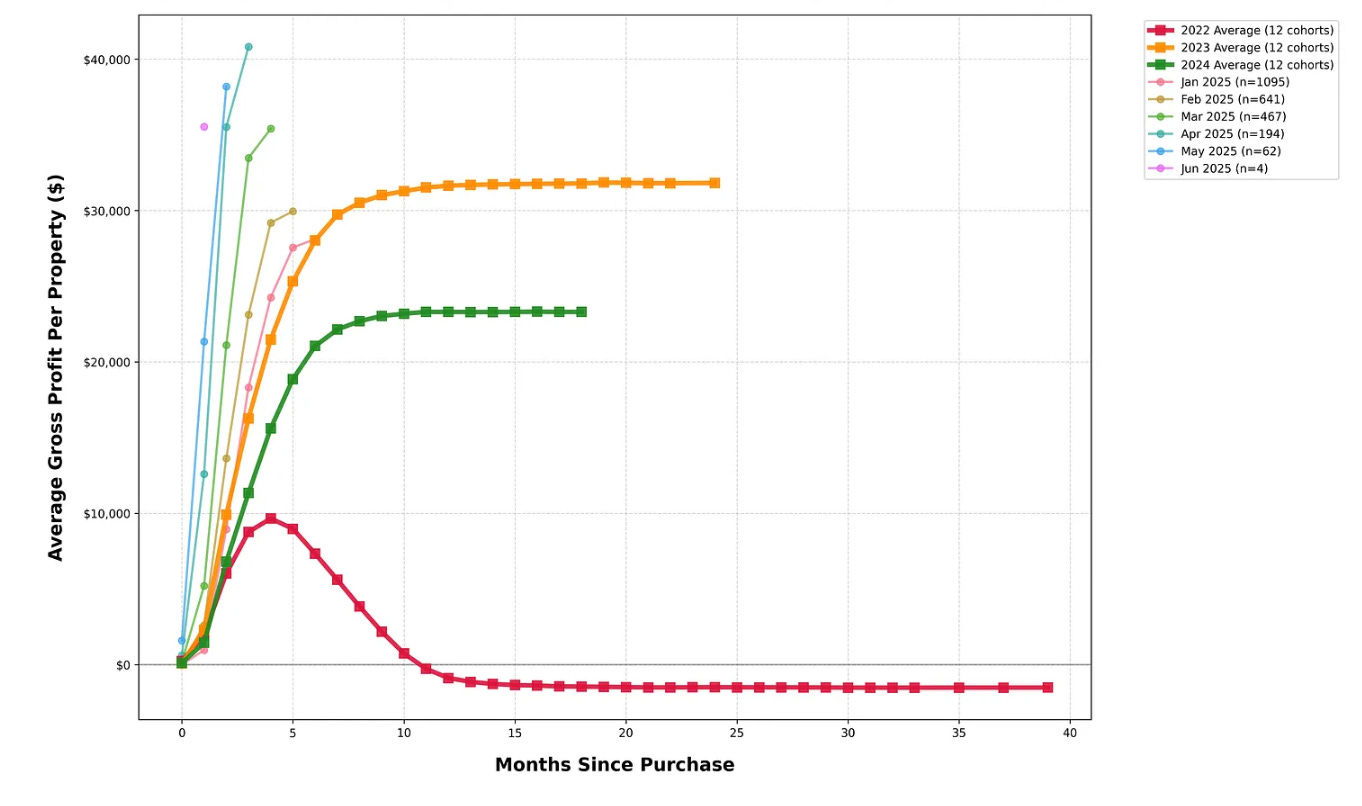

The above graph shows the gross margin over time for a given acquisition cohort. For example, in 2022, Opendoor on average made $10,000 for homes that they resold 0-4 months after purchase and then as hold times increased they made less and less profit until beginning to sell for lower than what they purchased for.

In 2023 they rebounded nicely, mostly by being much more selective in their acquisitions. When buying fewer homes, it’s easier to buy them for a better price. Once Opendoor started having positive gross margins, they began to steadily increase purchase volume throughout 2023.

With the real estate market facing headwinds, Opendoor couldn’t continue making the same margins they were in 2023 and began facing margin compression. Opendoor then stopped acquiring as many properties until late 2024, when they again started to ramp up purchases.

During this time, Opendoor’s stock continued to trend downwards. The company was unprofitable as a whole, and given the standstill in the broader real estate market there weren’t many things to get excited about.

That was until Eric Jackson wrote a twitter thread calling for a $82 price target on Opendoor in the next few years.

While we’ll let you decide the merits of the Twitter thread, there’s been a lack of clarity in some of the key metrics of Opendoor:

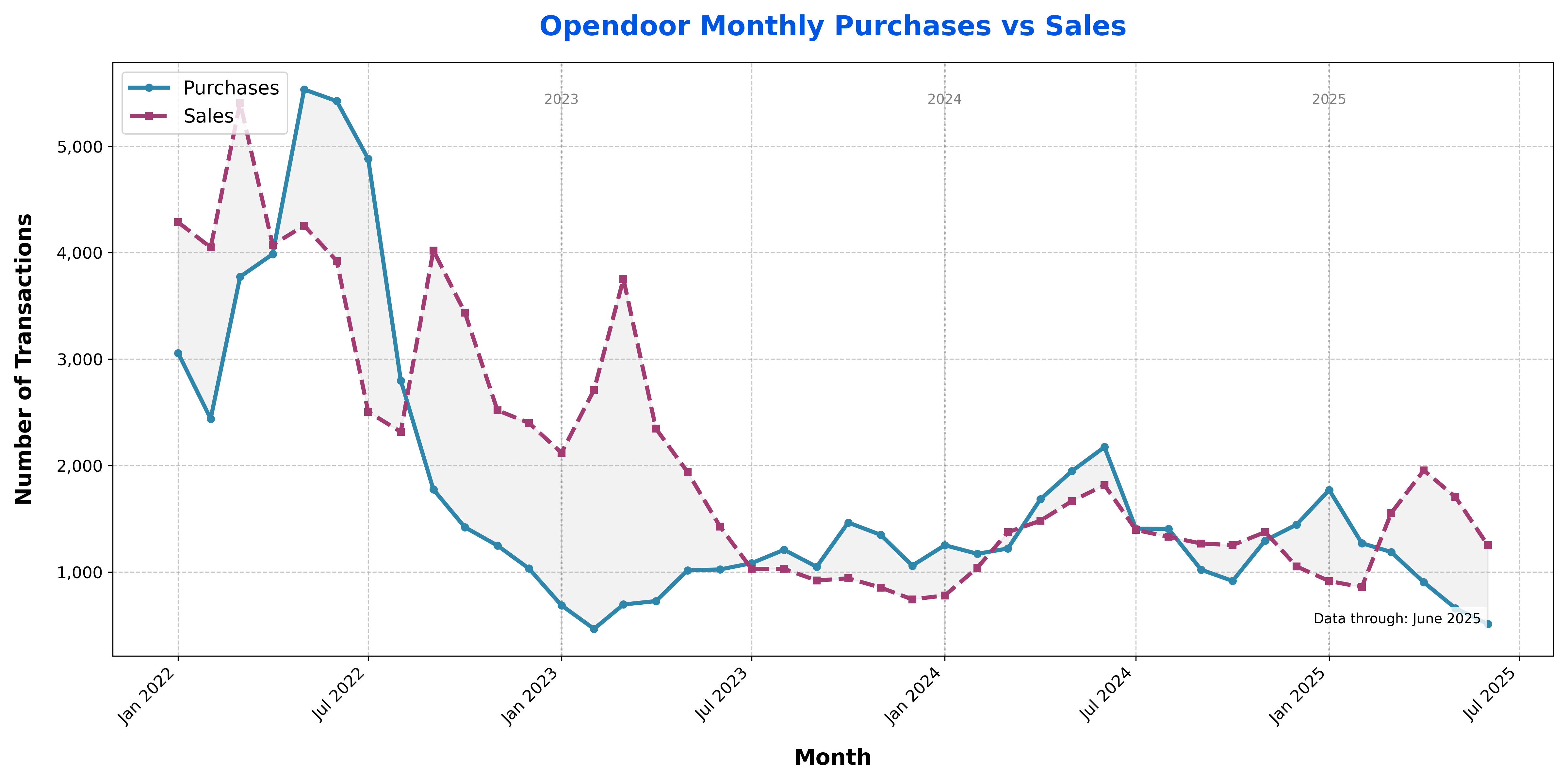

There’s a constant struggle to see if Opendoor can make good purchases while complete enough transactions to be profitable at the corporate level. While they’ve been operating in a difficult market, each time they’ve pumped acquisitions their gross margins have fallen before getting to profitability.

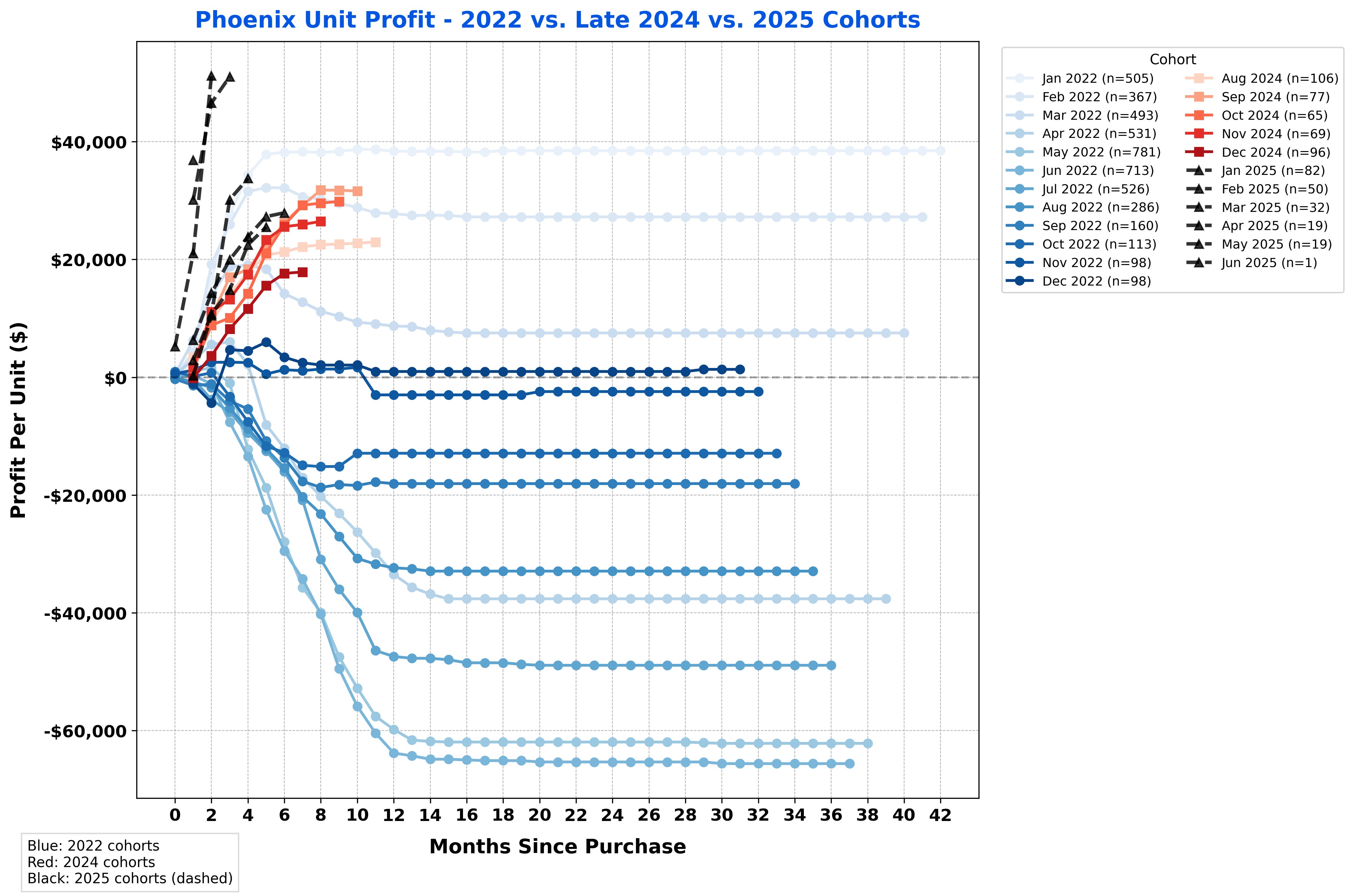

Opendoor isn’t nearly as bad at acquiring properties as some people make the company out to be. In 2022, Opendoor was — but since then the company has been consistently gross margin profitable. In Phoenix, which accounted for >50% of total losses in 2022, the last 12 months have routinely been between $20k-$30k gross margin profitable. As the company has laid off the risk in 2025 acquisitions, margins have also gotten stronger.

Right now, Opendoor is taking a risk-off approach. Their gross margins for acquisitions YTD are some of the highest they’ve ever been and they’re selling >2x more homes than they’re buying.

Overall - Opendoor is making better acquisitions, but not buying nearly enough to get to long term profitability. The question becomes when do rates come down and will that unlock enough transaction volume to grow significantly without facing margin compression.

Any add on notes on the 1) quarterly call 2) ceo exit 3) caretaker ceo 4) what next

Any updates to your analysis. There's been some significant changes at opendoor, worth noting and commenting on