Opendoor 2025: New CEO, Founder Return, and the "Opendoor 2.0" Pivot

Leadership shakeup, stock performance, and what transaction data reveals

Executive Summary

Opendoor bottomed at $0.51 per share in June before surging 20x to over $10 by September—sparked by Eric Jackson’s Twitter thread arguing for an $82 price target and the retail frenzy that followed.

After months of declining acquisition volume, the company has started to ramp acquisitions again.

Purchase price relative to Zestimate shows a strong correlation with gross margin performance.

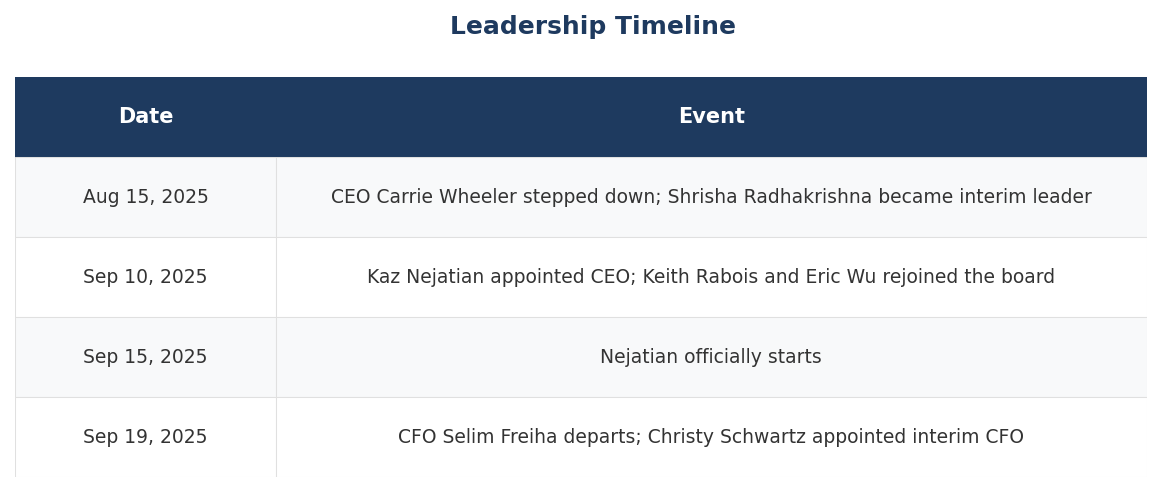

Leadership Shakeup: The Biggest Story of 2025

But the bigger story hasn’t been the stock price moves—it’s been the complete leadership reset.

The Timeline

Who is Kaz Nejatian?

Nejatian comes from Shopify, where he served as COO. Before that, he founded payments company Kash (acquired in 2017), then held product roles at Meta and Shopify. His compensation structure is notable: a $1 base salary, no cash bonus, and equity that vests only at specific stock price thresholds.

Founder Return

Perhaps more significant than the CEO change is the return of Opendoor’s co-founders to the board. Keith Rabois now serves as chairman, and Eric Wu (Opendoor’s original CEO) rejoined as a director. The company also announced a $40 million PIPE investment from Khosla Ventures and Eric Wu. This “founder mode” return signals a strategic reset—leadership now describes Opendoor as being “refounded” as a software and AI company.

“Opendoor 2.0” Narrative

In November 2025, Nejatian articulated a clear break from the past:

“We are refounding Opendoor as a software and AI company... making a decisive break from the past.”

This isn’t just marketing rhetoric. The company has launched several new products that represent a shift away from pure iBuying:

Key Connections: Connects partner agents with high-intent sellers (piloted Feb 2025, expanded June 2025)

Cash Plus: Combines Opendoor’s cash offer with the ability to list with an agent (launched July 2025)

Key Agent App: AI-powered tools for agent partners

The strategic shift is toward capital-light revenue streams and platform-based monetization rather than relying solely on home purchase spreads.

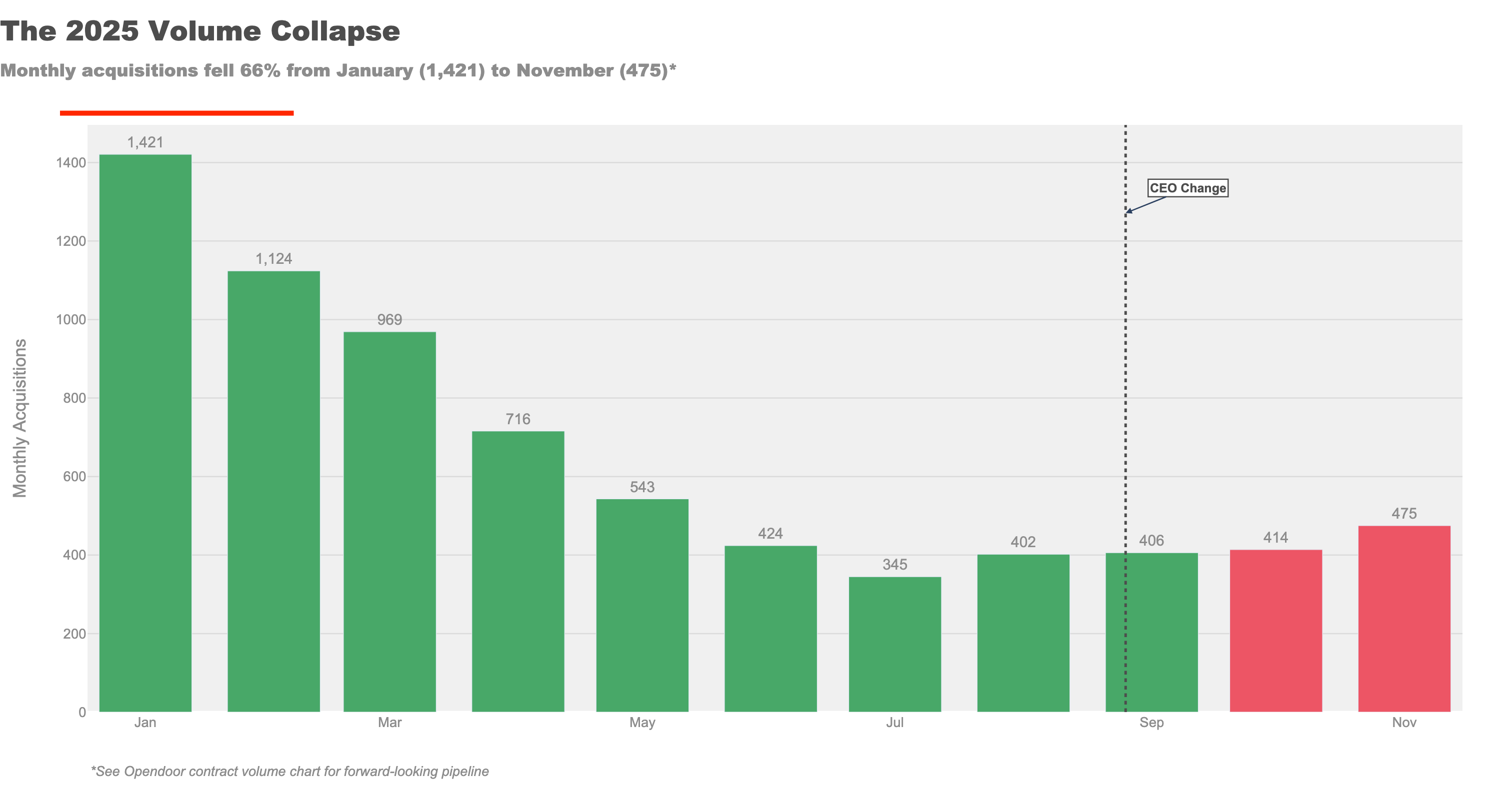

Acquisitions Are Beginning to Ramp

Acquisitions declined month-over-month through the first half of 2025, bottoming in August.

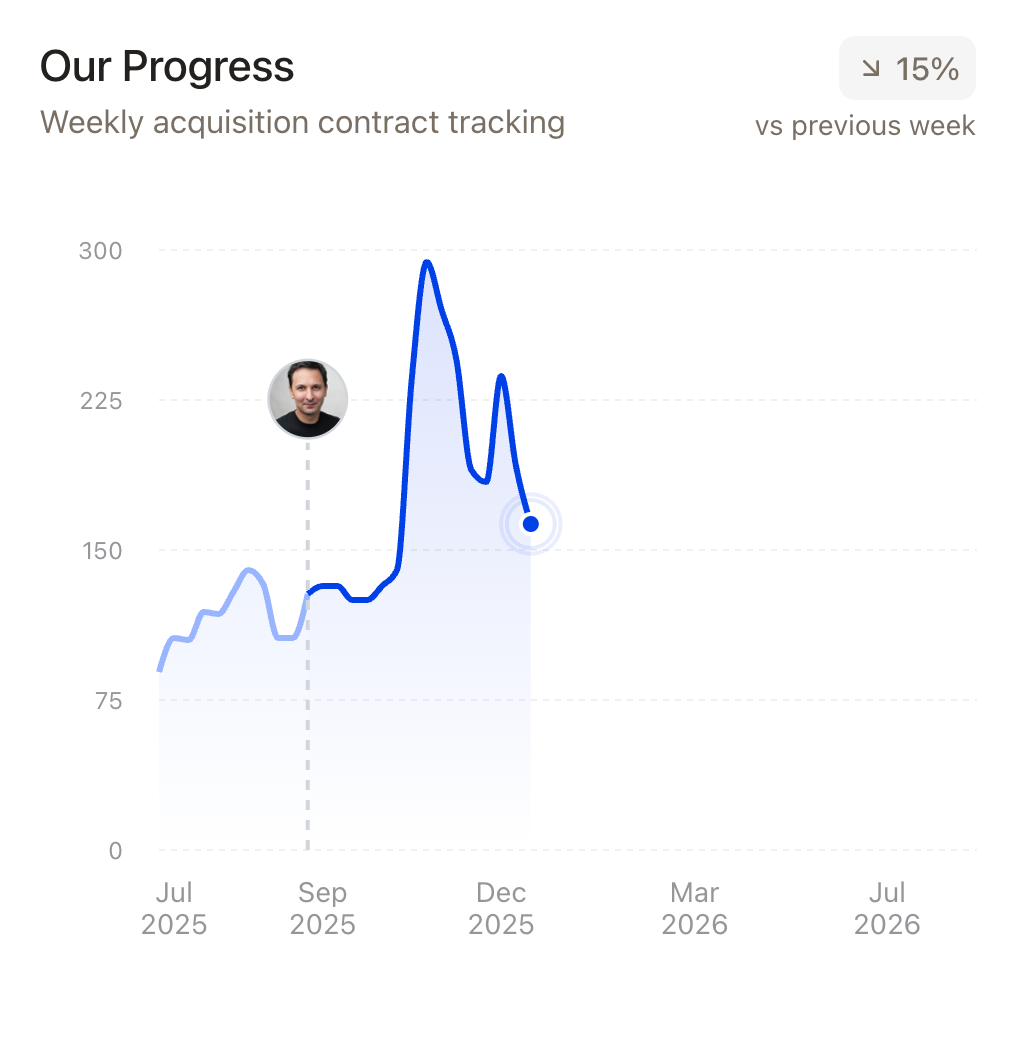

After several flat months, volume is picking up. Opendoor has started publishing weekly acquisition counts on its website—a signal that management expects the numbers to improve.

Note: Our data uses recording dates, which typically lag contract dates by a few weeks; some fallout between signed contracts and closed acquisitions is expected. Opendoor’s own progress tracker suggests volume approaching 1,000 acquisitions per month by January or February.

The key question: Can the company scale volume without sacrificing margin gains?

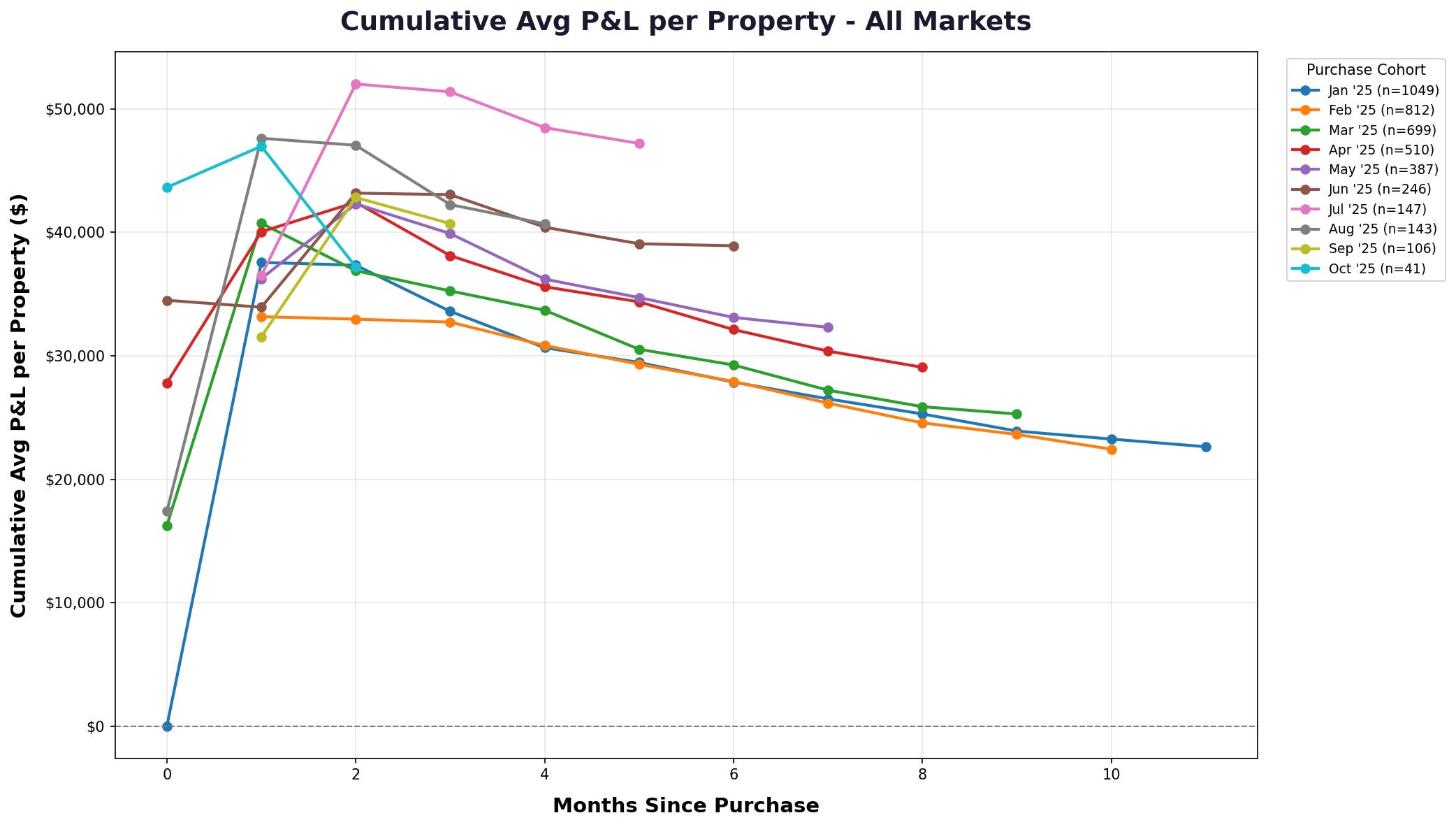

Average per-property gross margin in 2025, grouped by acquisition month, shows the pattern clearly: higher-volume months produced worse margins. As the buy box tightened in mid-2025, margins improved.

Management has long understood this dynamic: lower your margin requirements, and more sellers say yes.

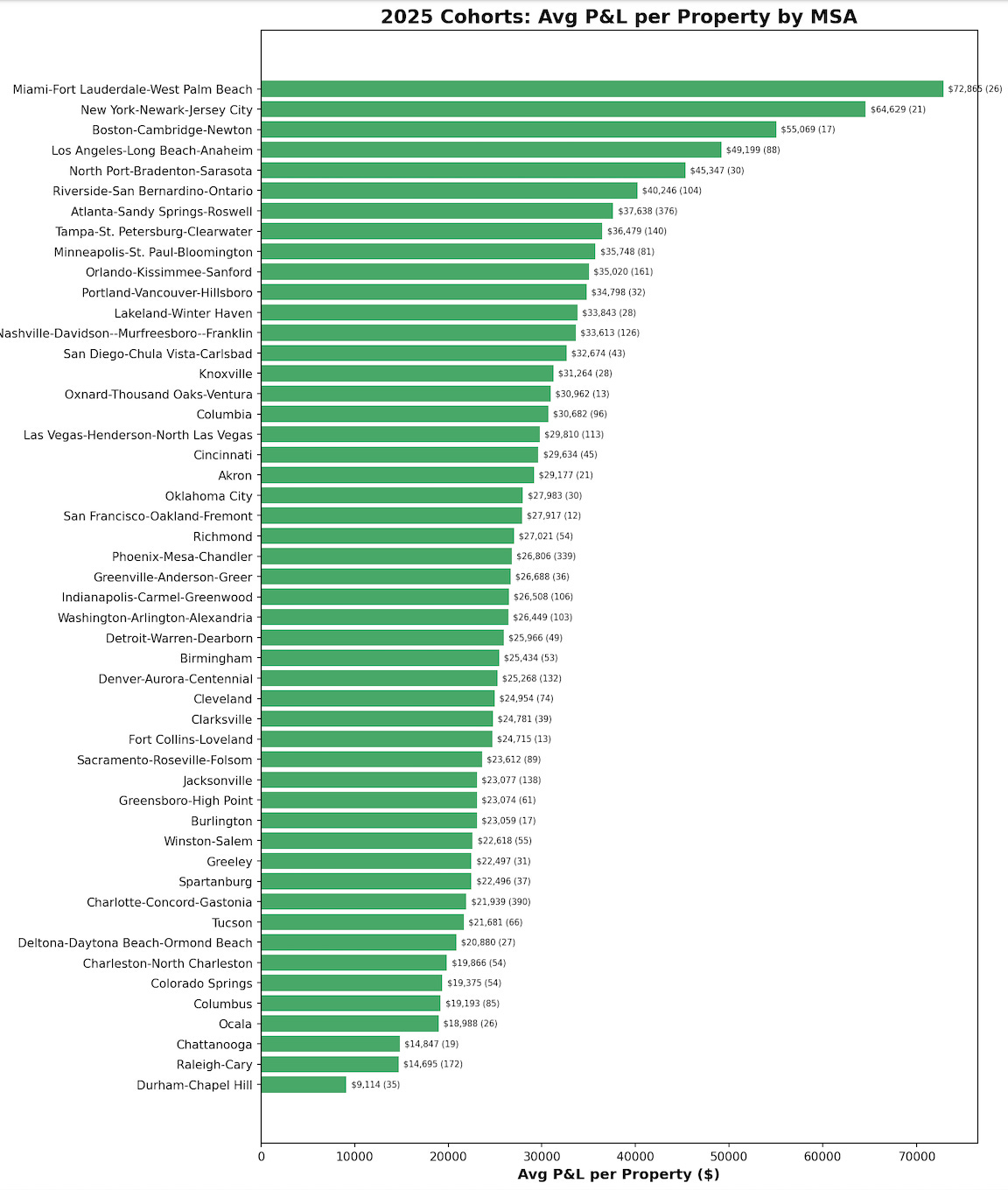

One way Opendoor plans to counteract this is by expanding to all markets in the lower 48 states. Instead of just concentrating on major markets, Opendoor is now giving offers throughout the country.

What remains to be seen is how they perform in new markets—performance by metro varies widely.

If Opendoor buys at a large enough discount in new markets, it can offset the risk of entering areas that are likely more difficult to operate in.

Expanding into more markets unlocks significant new demand, allowing Opendoor to increase acquisitions without necessarily sacrificing margin.

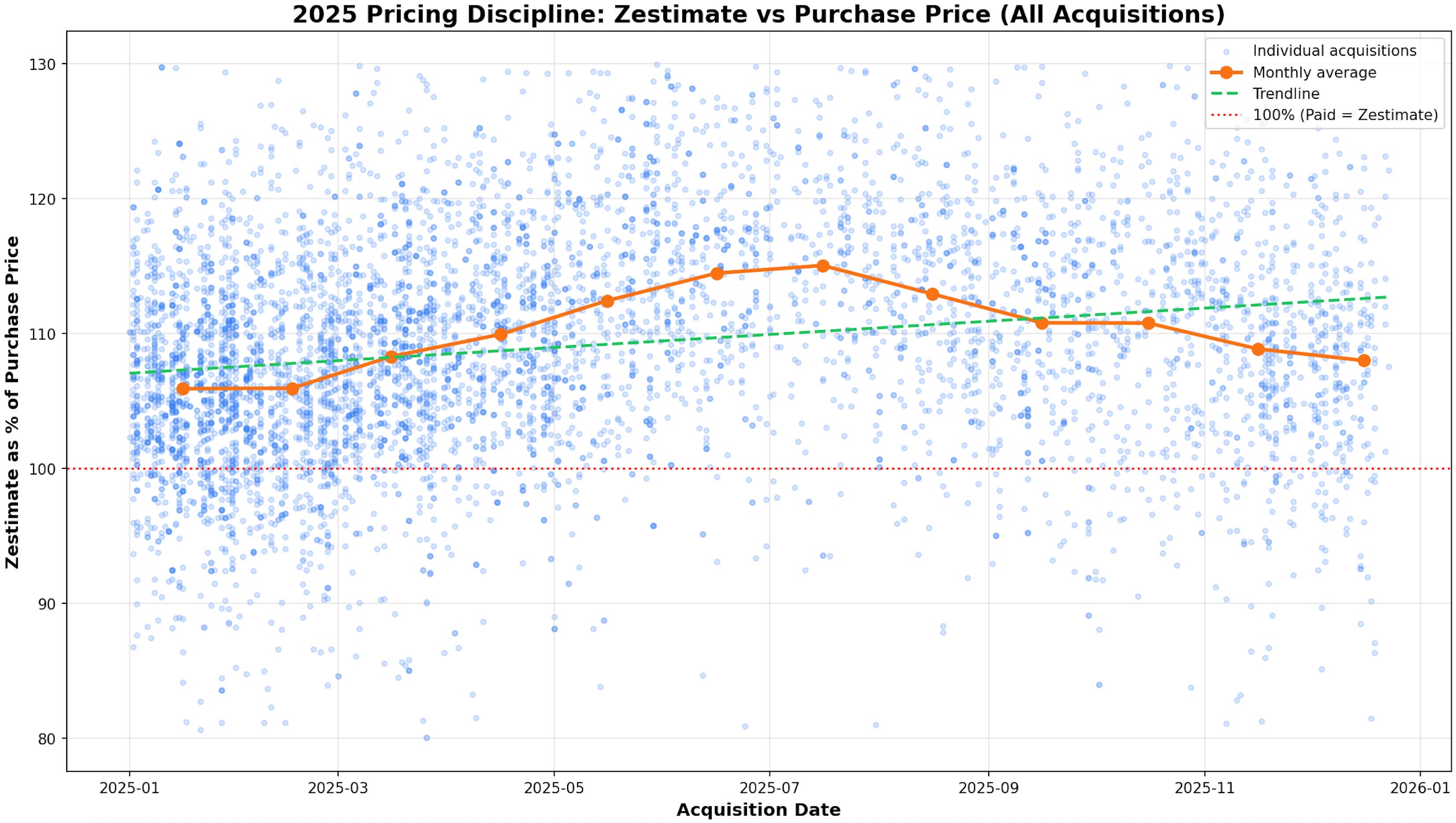

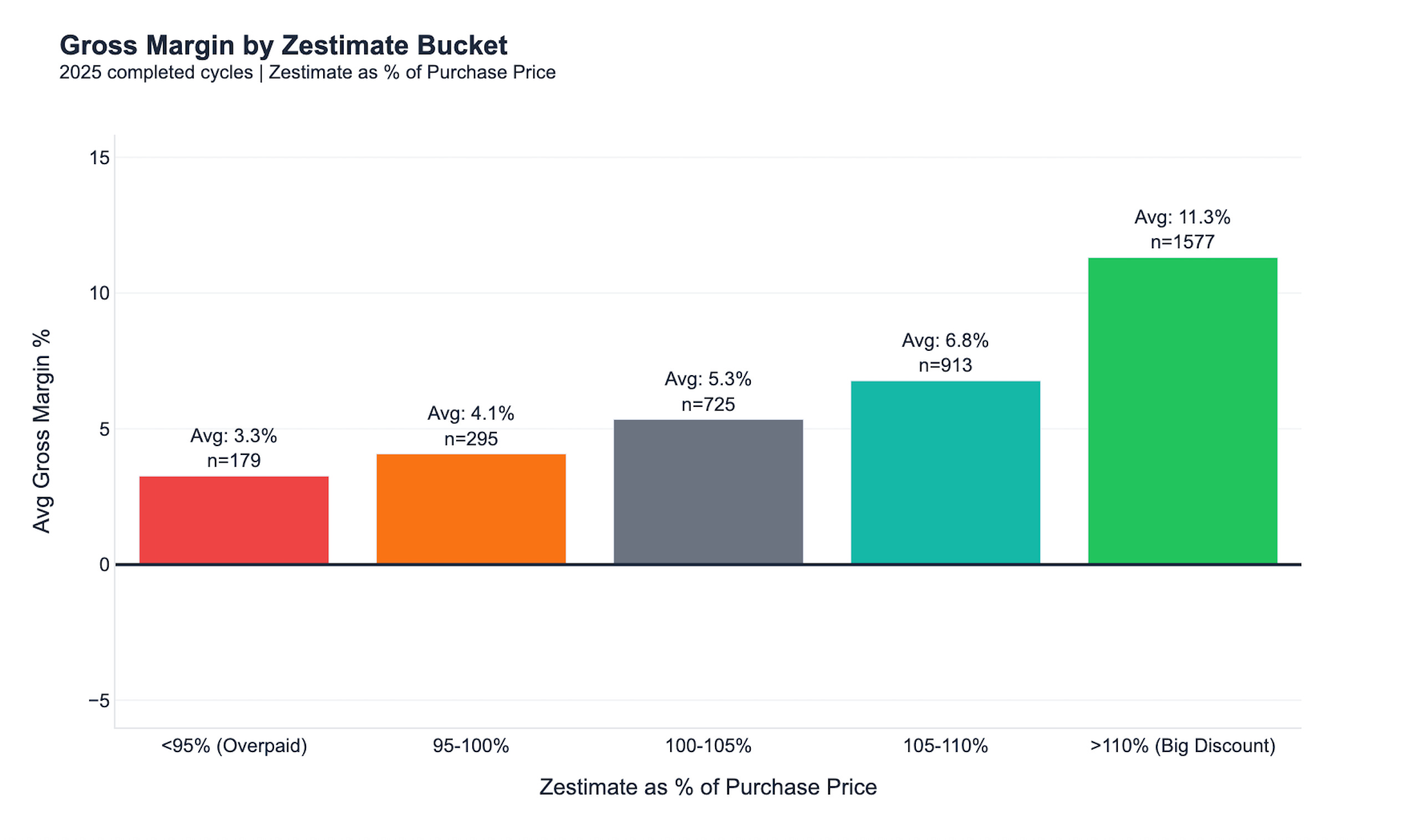

Performance Based on Zestimate

We benchmarked Opendoor’s purchase prices against Zillow’s Zestimate at the time of acquisition. It’s an imperfect AVM, but a consistent one.

As anticipated, the larger the spread between acquisition price and Zestimate, the better the gross margin.

While Opendoor clearly bought at deeper discounts in the first half of the year, that trend is now reversing. As Opendoor goes to increase acquisitions significantly, this will be key to watch to see if they’re relying on buying at less of a discount to increase volume.