California SFR Investment Report - May 2024

Rent growth changes, investor activity, and more.

Executive Summary

Across California, rent growth accelerated rapidly in 2021, reaching 8%+ year-over-year in many metro areas; in 2023, that trend reversed, with rent growth slowing significantly.

Inventory levels remain below pre-Covid levels across most of California.

California has been a popular state for large SFR operators, with an estimated 13,000+ single-family homes owned by institutional investors.

At the end of the article, a CSV showing detailed information about investor ownership in California for properties purchased during 2023 is available.

Data Overview

At SFR Analytics, we leverage nationwide deed and assessor data to track the single family rental market. To generate this analysis, we’ve:

Identified and reconciled the entities that SFR investors purchase properties under to have a complete picture of acquisition and disposition activity.

Cleaned and processed historical rental listings data to generate annualized growth rates based on paired listings.

Identified “Same Store” properties that have been listed and removed multiple times over the period studied.

Investors are defined as buyers who used a private lender or corporate buyers excluding trusts. We think this is the best proxy, but will underestimate investment activity from non-corporate cash buyers.

Analysis & Results

Monthly Inventory

Inventory levels remain below pre-Covid levels across major regions in California. There has been a small uptick in inventory from winter lows but time will tell if seasonal spikes will more closely resemble the muted summer months of 2023 or the explosive growth of 2022.

In regions like Sacramento, San Diego, and Anaheim, current inventory sits close to January 2022 lows, while markets like Los Angeles and Riverside have more robust inventory, but still lower than pre-Covid levels.

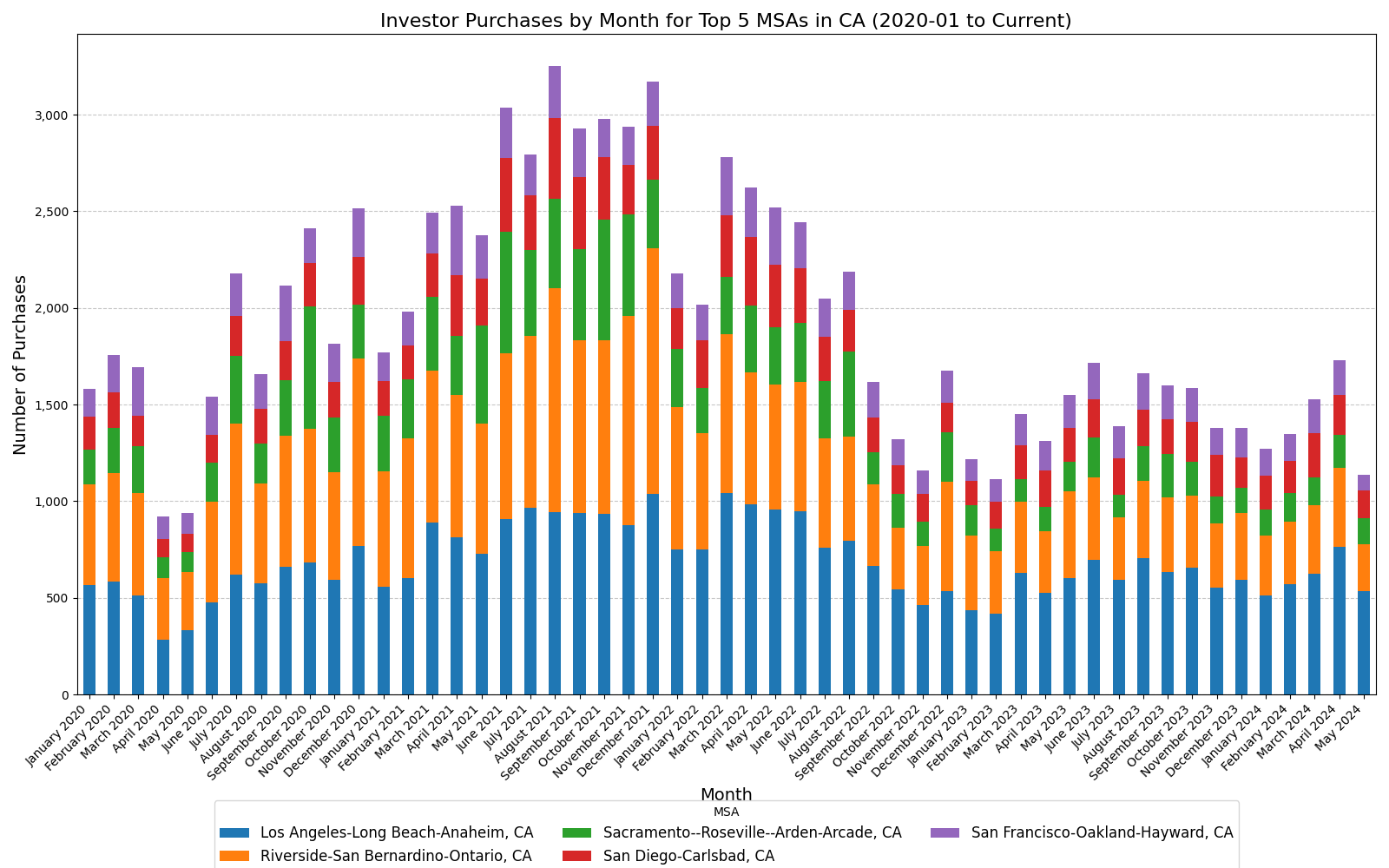

Investor Acquisitions

Investor purchase activity dropped sharply in March 2020 through June 2020 before roaring back to reach highs in late 2021.

Since early 2022, activity has since fallen significantly, with rising interest rates changing the math on prospective purchases. Both flipping activity and new rental acquisitions are down significantly.

There are three buyers that have purchase more than 100 properties year-to-date in California: Opendoor, Wedgewood, and Fair Trade. We’ve previously covered Opendoor and Wedgewood. Fair Trade is only a few years old but has quickly grown to become one of the largest players in residential real estate players within California. Fair Trade typically doesn’t hold the properties it purchases, instead double closing and quickly reselling the property to another investor. The company buys a large proportion of its deals via direct to seller acquisition, while also having strong relationships with wholesalers and agents who know that Fair Trade has an active network of investors looking to buy properties.

Outside of the top three buyers, there are roughly 50 buyers who have purchased 10+ homes year-to-date in California.

Note: the definition of investor purchase requires a corporate entity and ignores trusts, which frequently don’t reflect investor activity.

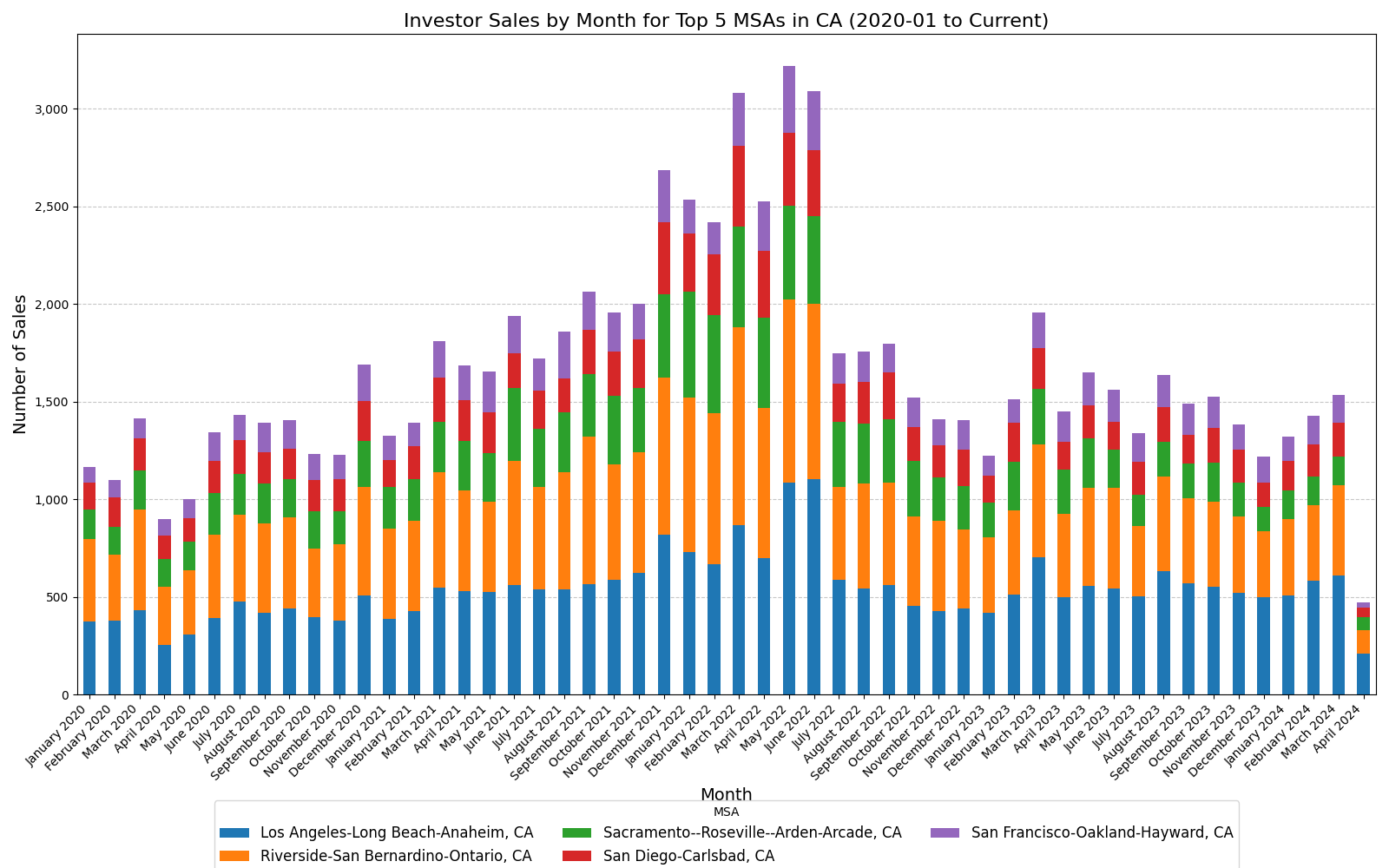

Investor Dispositions

Sale activity peaked in early 2022 and, like investor acquisition volume, has fallen significantly since. In early 2023, investor dispositions outpaced investor acquisitions during some months. Since then, investor acquisitions have outpaced dispositions.

Many of these investor dispositions are “natural dispositions” - often flippers exiting a property and selling it to an end user. Flipped properties often cycle from acquisition to disposition in 6-12 months.

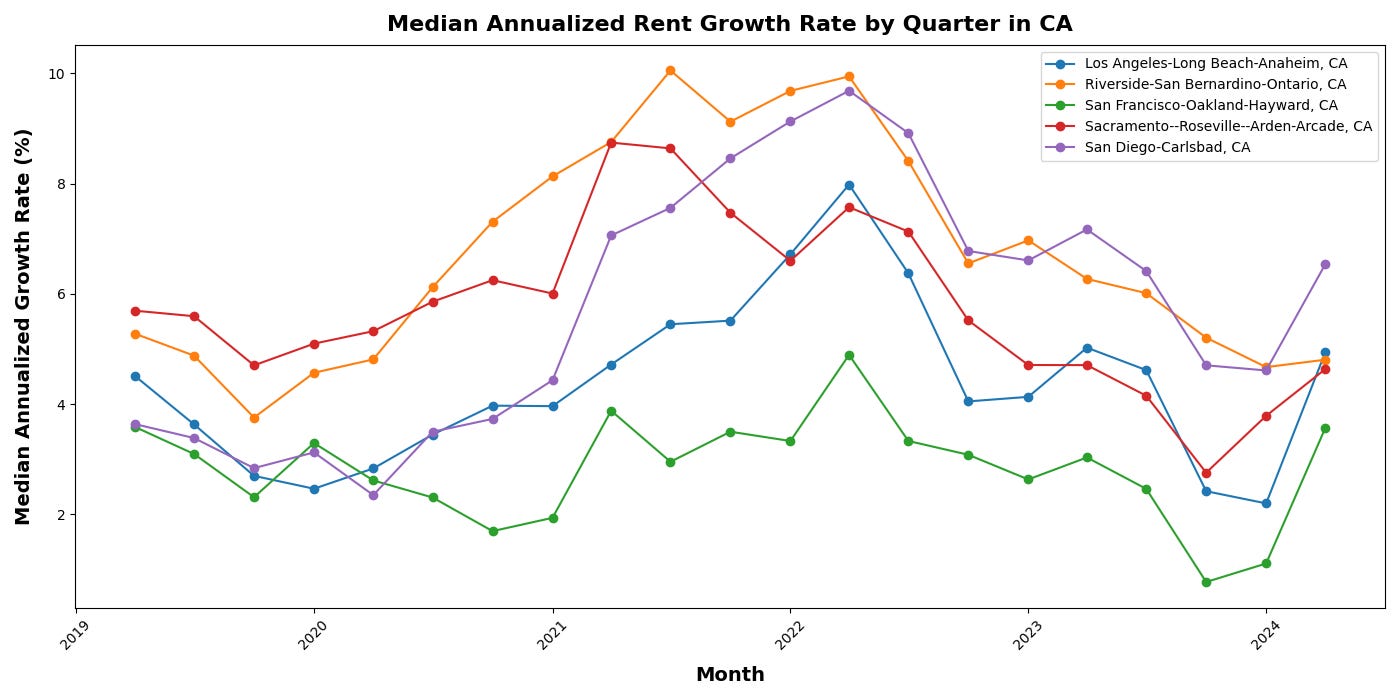

Rent Growth by MSA

Rent growth slowed significantly across California in 2022 and 2023 after rapid growth in 2021. However, growth has picked up in the spring season, with year-over-year changes in rental prices ranging from 4%-6%.

Private Lending Marketshare

Over the past 12 months, Kiavi has had the largest market share in California by a wide margin, accounting for over 12% of private loans compared to around 4% for the handful of next closest lenders.

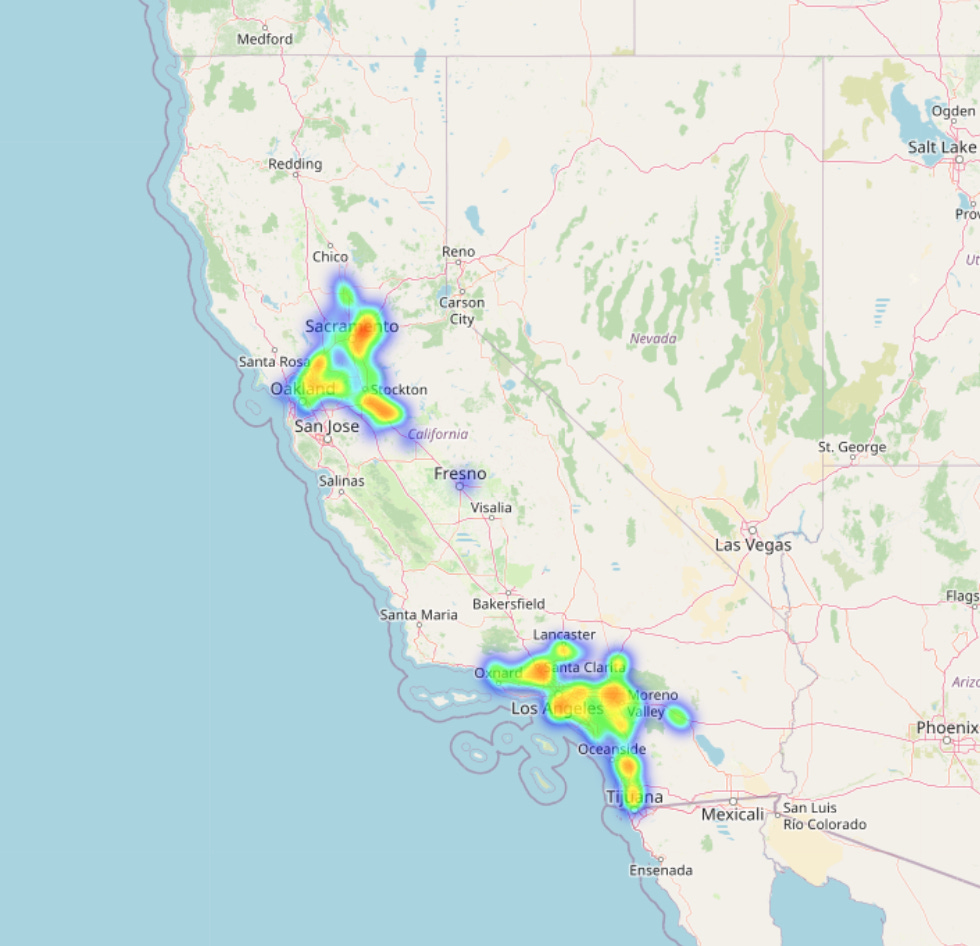

Institutional Ownership

Institutional investors have a heavy presence throughout California. We estimate that over 13,000+ single-family properties in California are owned by institutional investors.

Investor Ownership Details

While purchase volume is down from the heights of 2021, investors are still active in making acquisitions in California.

A full list of properties purchased by investors across California in 2023 is available below:

Note: the remainder of this article is available to paid subscribers, sign up below for access. Paid subscribers get full access to weekly data-rich articles about the SFR market and select additional articles only available to paid subscribers.